Accurately assessing property risk necessitates a clear understanding of how the surrounding environment is likely to evolve. Whether the concern is wildfire, flood, hurricane, or severe convective storm, risk is rarely static. As such, successful underwriting hinges on the ability to know what is happening around the asset and how those conditions change.

Developments in commercial Earth observation have significantly advanced what underwriters can see, how often they can see it, and how reliably they can compare it across time. The EarthDaily constellation, for example, has been designed around consistent,daily, science-grade measurement — calibrated for comparison across time rather than optimized for individual image capture.

The opportunity for underwriting is not simply more imagery. It is a more current, repeatable view of risk at the property level.

What Makes Geospatial Data Useful

Data is only useful if it can support a decision and that depends on the level of detail, the timing of the collection, and the reliability of the comparison.

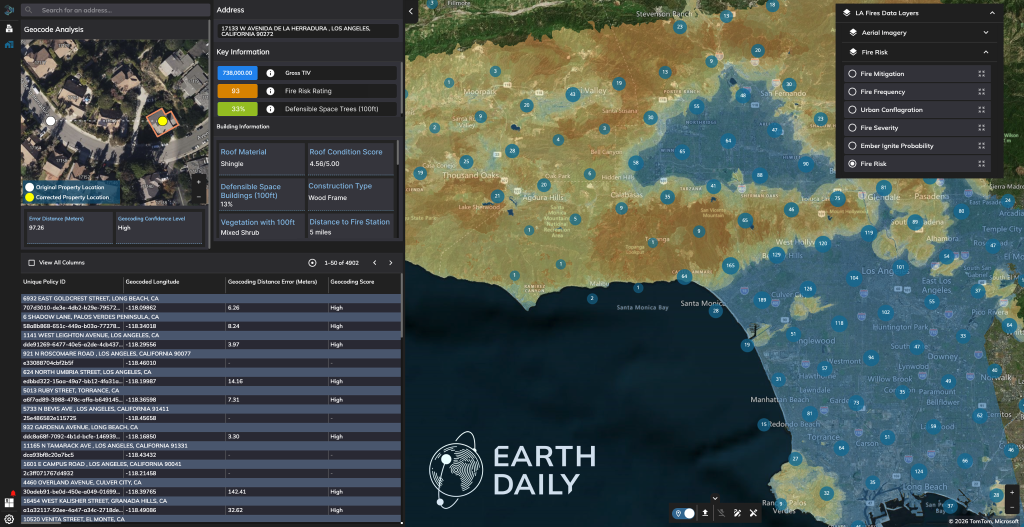

Traditional satellite datasets have often worked at 10 to 30 meters per pixel, a scale that is valuable for broad hazard assessment and portfolio-level modeling, but less effective when the underwriting question is specific to an individual property. At that scale, small details matter: the distance between a structure and nearby vegetation, the degree of impervious surface, whether conditions on the ground match what the file assumes.

Frequency of collection also impacts the usability of data. Many risk datasets are updated annually at best. In high-hazard areas, that can be too slow — particularly for wildfire risk, where vegetation, defensible space, and land management conditions can shift within a season. A more frequent revisit cycle allows carriers to monitor conditions across the policy lifecycle, not just at renewal or after a major loss.

But frequency alone is not enough. Reliable change detection requires consistency: images captured under varying viewing angles, illumination conditions, or sensor characteristics can create false signals or obscure real ones. The EarthDailys constellation is designed around repeatable collection geometry, calibration, and processing, so that comparisons across time reflect actual change, not measurement variation.

From Better Data to Better Decisions

Better underlying data does not automatically produce better underwriting decisions. The adoption gap is where many geospatial solutions succeed or fail. For underwriting, an insight has to be available when the decision is being made. A risk score that arrives after the policy is bound may still be useful, but it is not serving the same purpose.

It also has to fit into the way underwriting teams work. Carriers do not need another disconnected dashboard. They need signals that can feed into underwriting rules, models, review queues, and portfolio management processes.

Explainability is equally important. If a carrier uses a geospatial signal to adjust pricing, request mitigation, decline a risk, or route a file for review, the organization needs to understand the basis for that signal. What was observed? Where was it observed? When did it change? Why does it matter?

That gap between available insight and actionable decision is what environmental risk intelligence is designed to close. EarthDaily applies Earth observation data and analytics to help turn observed conditions into information that can support underwriting, claims, and portfolio decisions.

For geospatial intelligence to be operational, it has to be timely, integrated, and explainable.

EarthDaily’s geospatial visualization tool, Ascend, is purpose-built to surface property-level insights at-scale for underwriters.

What Precision Makes Possible

There is also a broader question of how better risk information is used. If the only outcome of more precise data is higher premiums and more non-renewals, the industry won’t grow.

The better opportunity is to use precision to support mitigation, conditional coverage, improved pricing, and product structures that reflect the actual characteristics of a location rather than broad assumptions about an area.

Carriers want to write business. The challenge in many high-hazard markets is that the available information has often been too broad, too static, or too outdated to support confident underwriting.

Geospatial intelligence can help close that gap. Its value is not only in seeing more detail but helping insurers understand risk with enough confidence to act, and enough transparency to explain why: to price more accurately, manage exposure more effectively, and keep coverage available where better information makes that possible.

Author bio – Margaret Williams

Margaret Williams is Director of Product Management for Insurance and Utilities at EarthDaily. She leads the development of data-driven solutions that support underwriting, risk assessment, and decision-making, with a focus on applying geospatial analytics to real-world insurance and infrastructure challenges.

Manufacturing & Engineering Magazine | The Home of Manufacturing Industry News