If you listen for too long to few influential but misguided voices (I won’t name them, but you know who I mean), you’ll probably have already accepted the conclusion that the UK North Sea is in a comatose state, eking out a slow death.

Of course, oil and gas reserves are in decline. This is true from day one of production in any field and, yes, the UK ceased to be a net exporter of oil and gas over 30 years ago.

But to (slightly mis-) quote Mark Twain, these reports of the North Sea’s death have been greatly exaggerated, despite being strangled by some of the highest tax rates and most stringent regulatory policy anywhere in the world.

Meanwhile, just further East of here, our near neighbours Norway continue to take a much more pragmatic approach to energy policy- backed by cross-party consensus- than their UK Labour counterparts.

While also pursuing ambitious climate goals, Norway continues to invest in, explore, and produce oil and gas, with a focus on low-emission production technologies. Maximising the economic and social value of the extraordinary resources that exist below our shared waters. Ironically exporting much of it to….eh, us.

And the truth is the UK could be doing the same but renewables progress in this country is beset by questions over investability, grid and storage capacity and a transmission charging regime that belongs in a different era.

The central flaw in the current approach is simple – the ‘transition’ is being treated as an act of replacement rather than an act of management. A clumsy, “let’s get from where we are now to where everyone wants to be in one almighty leap of faith” gamble. Instead of building bridges and mapping out a stepped approach, the reality is sadly more akin to lemmings on a cliff edge.

Check out the word transition in the dictionary. It’ll confirm the meaning as being “a change of state…over time”.

No serious person disputes the potential and growth of renewable energy. Offshore wind, solar, hydrogen, carbon capture and new technologies all have a major role to play.

We have built a world class industry around the North Sea, powered by some of the finest engineering minds and smart supply chain businesses. Skills and resources that have been coveted by but largely out of reach for other energy producing nations because they were fully deployed at home.

But we see real and worrying trends emerging that due to lack of traditional North Sea offshore work and the stalling of scale renewables roll out, these people and businesses are increasingly being lured overseas. Possibly never to return. Meaning that there will be no one here to build out and manage this next generation of energy projects.

The truth is Britain still relies heavily on oil and gas today and will do so for decades to come. The Climate Change Committee estimates that the nation will require circa 15 billion barrels of oil and gas equivalent to keep the country moving, our schools and hospitals running and our lights on at home between now and 2050. This usage is accounted for in their Carbon Budget and still enables us to achieve net zero targets. Currently, only around 4 billion of this will be produced in the UK, with the remaining 11 billion barrels being imported.

It has been estimated that the North Sea could economically produce 8 billion+ barrels. In addition to supporting the UK’s energy security, doing so would protect and create tens of thousands of jobs, provide billions of pounds of short term investment and tax revenues, growing GVA by around £165 billion. At a time the nation is crying out for growth.

So, the real question is not whether we use oil and gas during the transition, but whether we produce more of it ourselves under some of the highest environmental standards in the world – or import more from overseas supporting few UK jobs, paying no tax and with significantly higher global emissions. (It is interesting to note that gas from the, still mothballed, Jackdaw field is up to ten times less carbon intensive than the equivalent LNG we are importing instead).

Achieving a balanced fiscal and regulatory strategy should not be a difficult call, yet North Sea investment has been crippled by the Energy Profits Levy and a headline tax rate of 78%. Projects are being delayed and jobs are vanishing, at the rate of “a Grangemouth every fortnight” according to Robert Gordon University data. That’s 800 jobs gone and livelihoods ruined every month, many of them in Aberdeen. And for what?

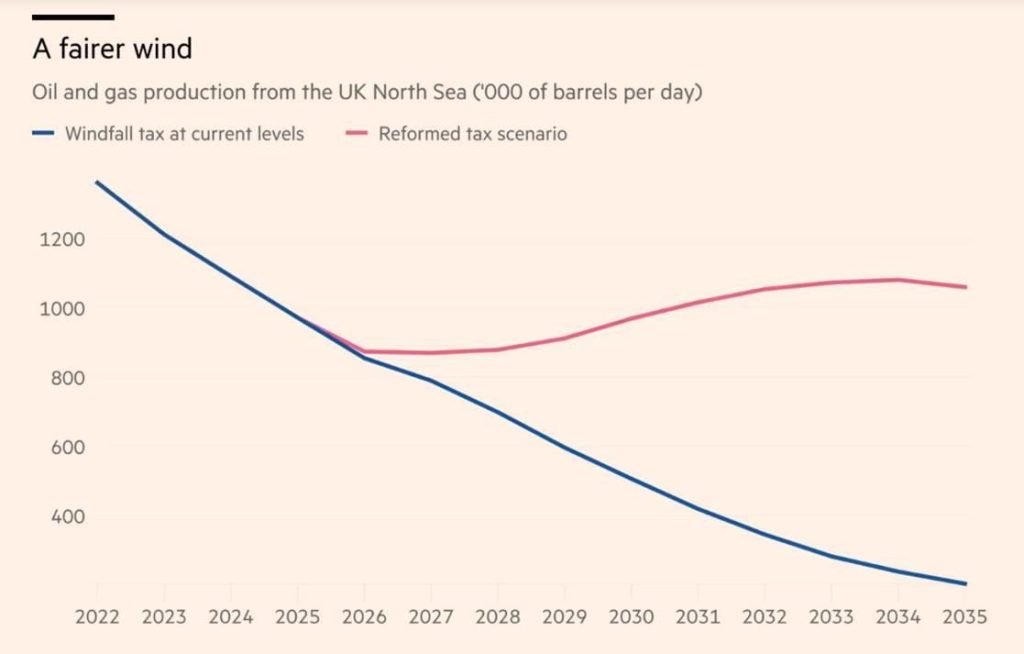

The government already has the answer. One that it announced in the 2025 Budget – the Oil and Gas Price Mechanism, a permanent and responsive windfall tax system that rises when prices spike and eases when they fall – but incredibly has been left sitting on the shelf until 2030. Too late. Triggering it now would give the Treasury revenue when genuinely exceptional profits occur, while giving investors the certainty needed to unlock £17.5 billion of near-term investment into Britain.

The prize is huge. An opportunity for the UK to demonstrate global leadership (again) with new energy. But we need pragmatism and a plan not just taking the plunge without first learning to swim in our offshore waters.

Fin out more by visiting www.agcc.co.uk

Manufacturing & Engineering Magazine | The Home of Manufacturing Industry News